The ‘biggest oil outage in history’ is a wake-up call for portfolio diversification, argues Ninety One’s Paul Gooden

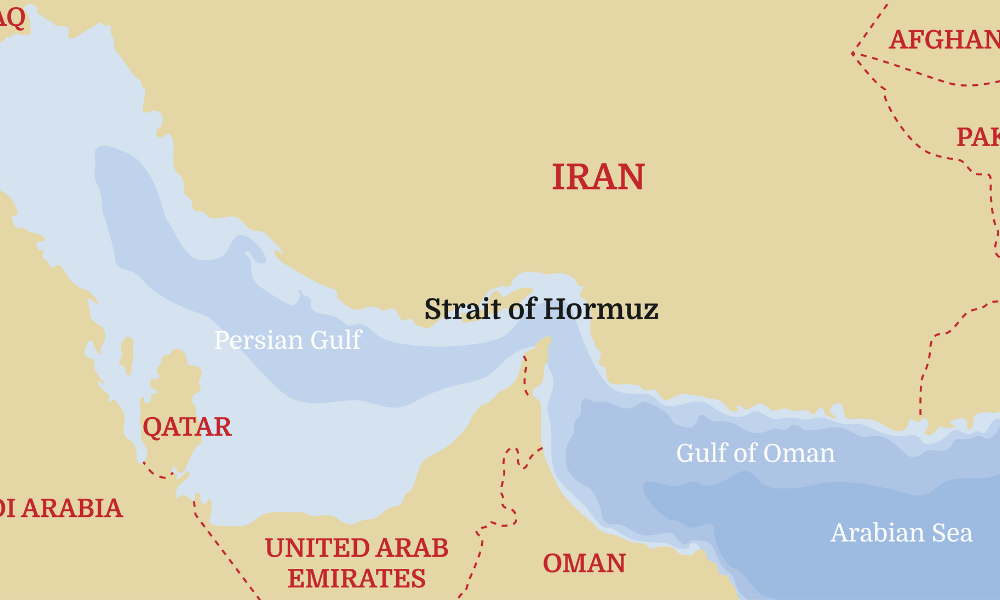

The closure of the Strait of Hormuz is the biggest oil supply disruption in history, and markets are only beginning to reckon with the consequences, all the while US President Donald Trump continues to make threats to have it reopened.

That’s why Paul Gooden is quick to highlight the scale of the outage dwarfs anything investors have seen before.

"This is the biggest oil outage in history. Roughly 20 million barrels a day of oil goes through the strait,” said Gooden, head of natural resources and a co-portfolio manager for the global natural resources strategy at Ninety One, adding while some redirection of flows and releases from strategic petroleum reserves (SPRs) have softened the blow, he estimates the net impact still sits around 12 million barrels a day - a staggering number in a 100-million-barrel-a-day market.

“The outage is so big on the supply side that inventories are getting depleted quickly. And the good thing about physical markets, physical commodity markets, is that the price solves. The price is there to make sure that supply meets demand, and the cure for high prices is high prices because that diminishes demand and, in theory, should create more supply. The problem is that in commodities, there can be quite a lag before that supply arrives.”

Gooden sees limited hope for a quick supply-side fix. In past shocks, US shale might have provided a fast supply response, but that option is weaker now because the sector is more mature and facing tougher geology. Even if US producers do respond, he thinks the increase will be modest, especially this early in the disruption. Five weeks in, the outage is still so large that the burden of rebalancing falls mainly on demand, not supply.

He sees demand destruction as slow and cumulative rather than sudden. Higher prices begin to curb consumption once oil moves above $100 a barrel, and the effect becomes more serious above $120, but it takes time to work through the economy. In the end, he believes the Strait of Hormuz will reopen, but the timing is highly uncertain.

To that end, Gooden believes markets might underestimating how long this lasts. He suggests Iran has a strong incentive to drag the process out because every extra day of closure tightens the oil market and increases pressure on Western governments through higher fuel costs, higher inflation risk, and the strain on consumers and borrowers. In his view, Iran may be able to withstand the political pain longer than Western governments can.

He's more cautious than market forecasts pointing to a quick ceasefire. Even if a ceasefire is reached sometime in May, he expects it would still take another month or two for oil flows to normalize, which would push the disruption into the Northern Hemisphere summer, when demand is seasonally stronger because of North American driving season.

More broadly, Gooden separates the issue into two horizons. The first is the next few weeks and months, where outcomes are highly event-driven and hard to forecast with confidence. The second is the more important strategic question: what this episode does to the longer-term oil price. He thinks the industry's assumed mid-cycle price needs to move higher, from around $70 a barrel to closer to $80.

He gives three reasons for that shift. First, governments are likely to rebuild and expand their strategic petroleum reserves after this shock, which would add meaningful demand over the next two to three years. Second, the world has now been reminded that Iran can threaten a major artery of global oil supply, so a lasting geopolitical risk premium has to be built into prices. Third, oil companies have spent a decade under pressure from investors to stay disciplined and avoid aggressive growth, so it may take a larger and more sustained rise in prices before management teams feel willing to spend more and increase output.

The result, said Gooden, is a world where consumers take the hit from both sides: directly through higher fuel prices and indirectly through inflation and interest-rate pressure. Whether central banks choose to look through that inflation shock or respond to it is, in his view, remains unclear.

“For Iran, this is a once in a generation opportunity to get what they want. And every day, the strait remains closed, the oil market tightens, Western consumers feel the pain, and Western mortgage payers feel the pain as well," he said.

Gooden sees energy equities as undervalued. At the start of the year, stocks were pricing in long-term oil in the low $60s a barrel; even now, he thinks they reflect roughly $70. If the mid-cycle price needs to sit closer to $80, as he argues, that leaves a meaningful gap.

Beyond oil producers, he highlights two other areas caught up in the disruption: fertilizers and aluminium. About a third of the world's nitrogen-based fertilizer production flows through the Strait of Hormuz and is now locked in, while a significant share of aluminium capacity in the region faces the same problem. Both industries are located there because of access to cheap energy, and both stand to see prices rise sharply.

According to Gooden, upstream oil companies and refiners are the clearest beneficiaries. Crude is relatively interchangeable, but as you move down the value chain into refined products, that fungibility breaks down by product type and geography, he explained. For example, jet fuel inventories, run far thinner than gasoline stocks, making refiners vulnerable to severe squeezes in specific product markets.

The picture is less straightforward for metals. Aluminium faces a direct supply hit from Middle Eastern capacity being shut in, but copper and iron ore are more exposed to the risk of a broader economic slowdown triggered by the crisis. Gold, despite a structural bull case Gooden still backs, has been held back by fears that persistent inflation will keep the Federal Reserve from cutting rates.

Yet, agriculture may carry the heaviest downstream burden, notably as higher fertilizer costs mean farmers use less, crop yields fall, and food prices eventually climb, noted Gooden.

He ultimately sees the crisis as a forced reckoning for asset allocators who have treated natural resources as a lazy underweight for two decades.

"I think it's a reminder that the ethereal world of the tech bros needs the material world of the natural resources industries," he said, underscoring how diversification really does matter.

"I think asset allocators really need to ask themselves, ‘Okay, in a higher inflation environment, how am I positioned for that? Because that's got pretty big portfolio implications," he said. "And then I think increasingly they need to ask this stagflation question as well."