Normandin Beaudry partner offers three possible paths for using surpluses

Most pension funds are currently in surplus but this won’t last forever, so this time of prosperity provides opportunity for pension plan sponsors to prioritize and implement strategies that could benefit their organization.

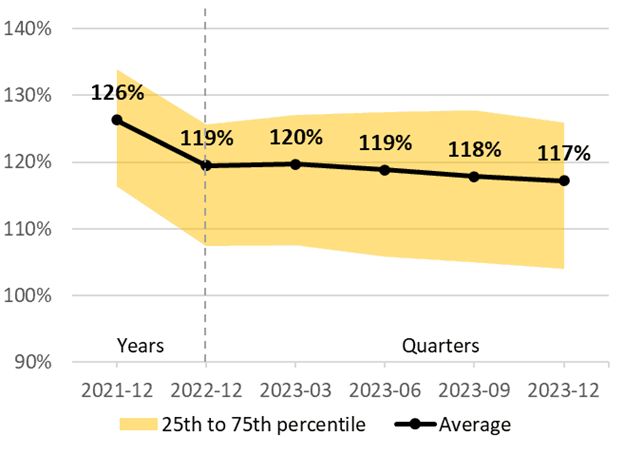

After a significant rise in interest rates in previous quarters, 2023 ended with slightly lower rates than at the beginning of the year. Despite the large variation of this key indicator, the financial position of the average pension plan remained relatively stable over the year, says Normandin Beaudry’s Pension Plan Financial Position Index, December 31, 2023.

The average pension plan funded ratio, excluding the effect of asset smoothing, is 117 percent as at December 31, 2023, down one percent in the fourth quarter and down two percent since the beginning of the year.

Note: The illustrated funded ratio excludes the effect of asset smoothing. A plan that uses this mechanism can therefore expect less significant change in its financial position.

“The key message here is pension plans look good, they're in surplus right now, and they might not be there forever,” says Pierre-Luc Meunier, partner, pension and savings with Normandin Beaudry. “So, what are you, as a plan sponsor, doing with your surpluses right now? Are you acting on them? Are you taking some measures and what are those measures?”

Meunier says these are the questions his firm is discussing with clients right now.

Three paths to using surpluses

“There are three different paths to using those surpluses,” he says. “Path number one would be for some employers to take contribution holidays. And some employers say, ‘Well, we've put in so much money over the past 10, 15, or 20 years because there were large deficits, now that we're in a surplus position and we're allowed to do it, we can take a contribution holiday.’

“The second path would be to derisk, because plans may have taken risks in the past, and some risks do pay off, but some risks do not pay off or tend to be bring some volatility. So, is it time to reduce volatility in the plan? With higher interest rates, there's an opportunity to reduce exposure to some asset classes that are riskier and take less risk while still achieving good returns. Fixed income would be an example. Many sponsors consider fixed income as one way to derisk. Another way to do it is to purchase annuities and transfer risk to insurers.

“The third path is ‘what can we do with our benefits?’ We've seen a lot of conversation around inflation. If inflation is high, how does that affect members? There are other conversations as well. There is a huge labour shortage in many industries, and this is the opportunity to use those surpluses to adapt the pension plan to current context.”

Plans may look at how to introduce flexibility into the plan design or how to improve equality, diversity, and inclusion (EDI).

“We are following decades of plans in deficit where we had completely different realities,” says Claude St-Laurent, principal, pension and savings at Normandin Beaudry. “Right now we have surpluses and they might not be there forever.”

Strategic suggestions for surpluses

The Pension Plan Financial Position Index offers some strategic suggestions for pension plan sponsors to consider for their surpluses under three headings: investments, funding, and benefits. St-Laurent says it is not an exhaustive list, but it gives sponsors a place to start considering what they could do.

“Companies must prioritize, but the first step in order to prioritize is just to know what's out there,” he says. “It's an important decision and decisions can have repercussions in the long term. So, it's better to take the time to take a step back and decide.”

He adds that implementing any strategies can take some time, another reason to take advantage of this time while in surplus. Sponsors will need to adhere to their plan text and take the proper steps to make changes.

Additional data from the Pension Plan Financial Position Index include:

- The average funded ratio was 117 percent as at December 31, 2023, down one percent over the fourth quarter and down two percent since the beginning of the year.

- The average solvency ratio: 110 percent as at December 31, 2023, down one percent over the quarter and up three percent since the beginning of the year.

- There were positive returns in the fourth quarter and over the year 2023, in both stock and bond markets.

- The going concern and solvency discount rates in the fourth quarter dipped to levels slightly lower than at the beginning of the year, resulting in an increase in liabilities and current service costs.

Is your plan in surplus? Tell us what your organization is considering, if anything, to do with that surplus. Comment below.