Defined benefit plans are in good health with opportunities to use surplus - but they should prepare for risks ahead – Mercer

With more defined benefit (DB) plans showing solvency ratios of more than 100 percent than at the beginning of the year, now is a good time to review risk management profiles and frameworks on what to do in the event of adverse scenarios, says Jared Mickall, Mercer Winnipeg office wealth practice leader, pension consultant, and actuary. “In other words, we recommend that pension plan sponsors don’t become complacent.”

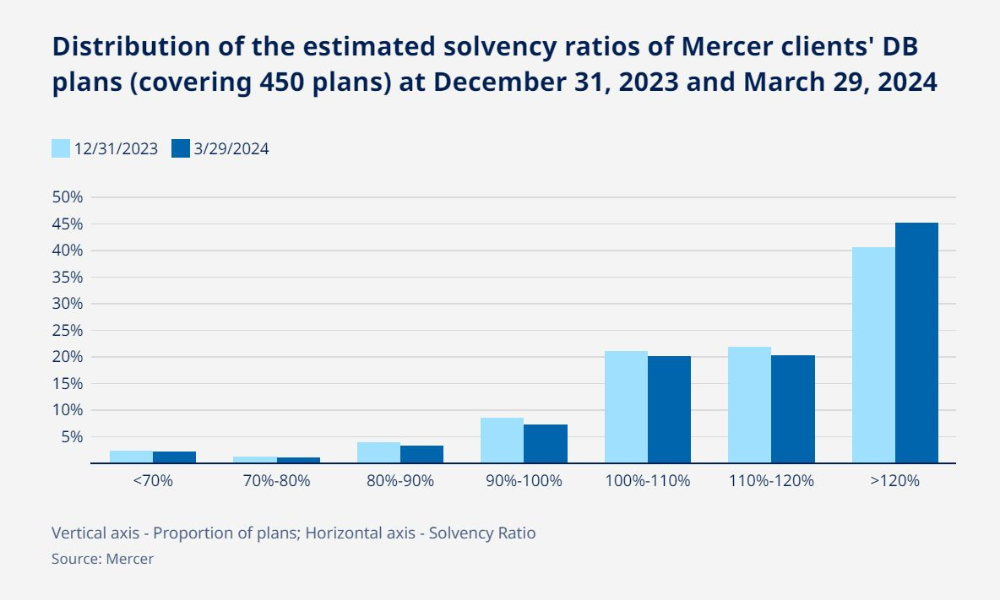

The Mercer Pension Health Pulse (MPHP), a measure that tracks the median solvency ratio of the defined benefit (DB) pension plans in Mercer’s pension database, shows an improvement in March over December. The solvency ratio is 118 percent as at March 29, up from 116 percent at December 31, 2023. The solvency ratio is one measure of the financial health of a pension plan. This financial health puts plans in good standing as new risk management guidelines from Canadian Association of Pension Supervisory Authorities (CAPSA) are due to be released this year. In addition, compared to the beginning of year, there are more DB pension plans with solvency ratios above 100 percent.

Throughout the first quarter, most plans saw positive asset returns coupled with decreased DB liabilities, which resulted in an overall strengthening of solvency ratios. DB pension plans that used fixed income leverage may have experienced stable or improved solvency ratios over the quarter. But Mickall says plan sponsors should resist complacency, and take this opportunity to revisit risk management practices, and prepare for potential adverse financial events.

Solvency ratios raised by strong equity performance

“Members of DB pension plans likely saw continued improvement in the financial health of their plans over the first quarter,” he says. “Solvency ratios were raised by strong equity performance and interest rate increases.”

Canadian inflation eased to 2.9 percent in January, which is less than the upper end of the Bank of Canada’s inflation-control target of three percent. It is the Bank of Canada’s expectation for inflation to remain close to three percent during the first half of 2024 before gradually easing. On March 6, the Bank of Canada continued its policy of quantitative tightening by maintaining the overnight rate at five percent. On March 19, Canadian inflation for February 2024 came in at 2.8 percent, which ignited industry speculation on the timing and amount of a cut to the overnight rate.

Although the overnight rate remained unchanged during the first quarter, interest rates on Canadian bonds with longer terms finished the quarter at levels greater than they were at the start of the year. Due to the long-term nature of DB pension plans, long-term interest rates pose a significant risk for many DB pension plans. Monitoring long-term interest rates on Canadian bonds as well as the overnight rate, would be an ongoing focus for DB pension plan stakeholders.

“While the overnight lending rate was maintained at five percent, interest rates rose for defined benefit plans when it comes down to how they value their liabilities,” says Mickall. “The cash flows that are expected to be paid from these plans are paid out over a much longer time horizons into the future than the overnight lending rate. Most pension plans discount their cash flows using bond yields at five years, seven years, 15 years, and even longer. And so, it is those interest rates that we saw that had increased over the quarter that then resulted in liabilities, declining in light of the fact that the overnight lending rate remained unchanged.”

For DB pension plans in the enviable position of enjoying a surplus, having an effective strategy for its use should be on the agenda. Contribution holidays, improving benefits, or retaining surplus are typical options and their financial impacts should be explored.

Pension plan risk review is prudent

When considering the current financial strength of a DB pension plan, given the risk of a decline to Canadian interest rates and ever-present market volatility, a review of a pension plan’s risks to be retained or transferred (e.g. annuity purchase) continues to be prudent alongside the approach to surplus usage. The MPHP says that while a strategic annuity purchase is top of mind for many DB pension plans, a tailored investment strategy is a viable, and in some cases the only feasible, alternative to annuitization. A regular review of a pension plan’s investment policy continues to be appropriate and such reviews may be expanded to include sustainable investment beliefs.

“While it is likely that solvency ratios have improved, Canadian DB pension plans should take the opportunity to be strategic on their use of surplus and are advised to be steadfast in the financial management of their plans and avoid becoming complacent,” says Mickall. “Canadian DB pension plans should take the opportunity to revisit their risk management processes in anticipation of new guidelines from CAPSA. Canadian DB pension plans should also prepare for adverse financial experience. Understanding the risks associated with interest rate changes, market volatility, increasing longevity, plan maturity, and other risks specific to each DB plan are necessary for a DB plan to meet its long-term objectives. Applying appropriate governance and risk management processes should set a clear path forward.

“We expect the upcoming CAPSA guidelines will cause plan sponsors and administrators to revisit their policies just to understand how they fit and see if they need to be updated to accommodate these new frameworks.

“The nice part is that taking the time to undergo a risk management review is a bit more comfortable when the financial strength of the plan is positive.”