A group registered retirement savings plan allows you to build your nest egg through payroll deductions. Find out if this strategy suits your financial goals

If you have access to a group registered retirement savings plan (RRSP), this can serve as an important tool to help secure your financial future. A group RRSP is a work-sponsored savings plan that helps you build your retirement nest egg with contributions directly deducted from your paycheque. Employers also have the option to match these contributions, potentially giving your retirement income a huge boost.

In this article, Benefits and Pension Monitor walks you through how a group RRSP works. We will discuss the different elements of the plan and how they can impact your retirement savings. We will also give you a breakdown of a group RRSP’s pros and cons.

Whether you’re just starting your career or planning for retirement, understanding how to maximize the benefits of a group RRSP can put you ahead of the game. Read on and find out how a group registered retirement savings can help you build a stable financial foundation for your future.

To the industry professionals who typically visit our website, this guide is part of our client education series and can be a good resource to send to your clients.

What is a group registered retirement savings plan?

A group RRSP serves as a savings and investment program set up by your employer to help you save for retirement. Think of it as a workplace benefit that makes it easier to build your retirement nest egg. Contributions are deducted automatically from your paycheque, making the process simple and convenient. You can also get immediate tax benefits as these contributions are made before income taxes.

Group registered retirement savings plans function mostly like individual RRSPs. The main difference is that group RRSPs are managed by your employer, who has the option to match your contributions.

Another valuable tool to help you prepare financially for retirement is the Canada Pension Plan (CPP). Find out how the plan works in this guide.

How does a group RRSP work?

Because group registered retirement savings plans are sponsored by the company, they may also work differently depending on the employer. Some businesses offer group RRSPs only to staff who have been employed for a certain number of years.

Generally, participation in your company’s group RRSP is optional. As mentioned, once you decide to join, contributions are made automatically through payroll deductions. You also have control over the investments, allowing you to build a portfolio suited to your financial goals.

These are the key elements and features of a group registered retirement savings plan that you need to be aware of:

Contributions and contribution room

Group RRSP contributions are deducted straight from your paycheque. Apart from being simple and hassle-free, this payment structure encourages discipline in financial planning and removes the common barriers that come with just setting aside funds.

The contribution room for your group RRSP is combined with those of the other RRSPs you may have. This means that the total amount you can put into your plan depends on your overall RRSP contribution limit. The annual limit is 18% of your previous year’s earned income, up to a maximum set by the Canada Revenue Agency (CRA). For 2024, the annual RRSP contribution limit is $31,560.

You can carry over any unused contribution room from previous years. This gives you the flexibility to contribute more when you can afford it.

Be careful, however, of exceeding the annual limit. If you do, the CRA will charge you a 1% monthly penalty for overcontributions of more than $2,000. The tax penalty continues until the amount is withdrawn or your limit covers the excess contribution.

Tax benefits

Contributions are deducted before income taxes are calculated, reducing your taxable income right away. This immediate tax benefit can make a big difference in your take-home pay, putting more money back in your pocket while you save.

The funds in your group registered retirement savings plan also grow tax-free until you withdraw them. This allows your investments to compound more effectively over time.

While group RRSPs are designed for retirement, they also let you withdraw funds any time, although these will be taxed as income. Also keep in mind that withdrawing early reduces your retirement savings and available contribution room.

Employer matching

One of the biggest advantages of a group RRSP is employer matching. Your employer may offer to match a percentage of your contributions. If they do, this essentially means “free money” going towards your retirement fund. Let’s say your employer matches 50% of your contributions up to a certain limit. Every dollar you contribute then turns into $1.50. By increasing the contributions, employees are incentivized to participate in the program.

Some plans, however, come with a vesting period. This requires you to be employed for a certain time frame before you can fully own the employer’s contributions. Be sure to check your plan’s details to understand how this works.

Investment options

Group registered retirement savings plans provide a range of investment options, including mutual funds, stocks, and bonds. You can choose from conservative, balanced, or aggressive investment strategies based on your risk tolerance and retirement goals.

Most group plans also have lower management fees compared to individual RRSPs. On the flip side, individual plans provide more diverse investment options.

Plan portability

If you change jobs, you can usually take your group RRSP with you. You often have three options when it comes to transferring funds without triggering taxes:

- to another RRSP

- to a locked-in retirement account (LIRA)

- to another registered plan, including the registered retirement income fund (RRIF)

The funds can also be used to buy annuities. You can also take them with you as cash, but they will be subject to income taxes in the year you receive them.

Spousal RRSP

Group registered retirement savings plans offer the option of spousal contributions. This can be a strategic way to balance retirement income between spouses, especially if one earns significantly more. This option also helps reduce taxes by allowing income splitting during retirement.

Spousal contributions, however, still count against the contributing spouse’s RRSP room. That’s why it’s important when taking this route to plan your contributions accordingly.

Check out this guide on how your employer chooses benefits plans for employees.

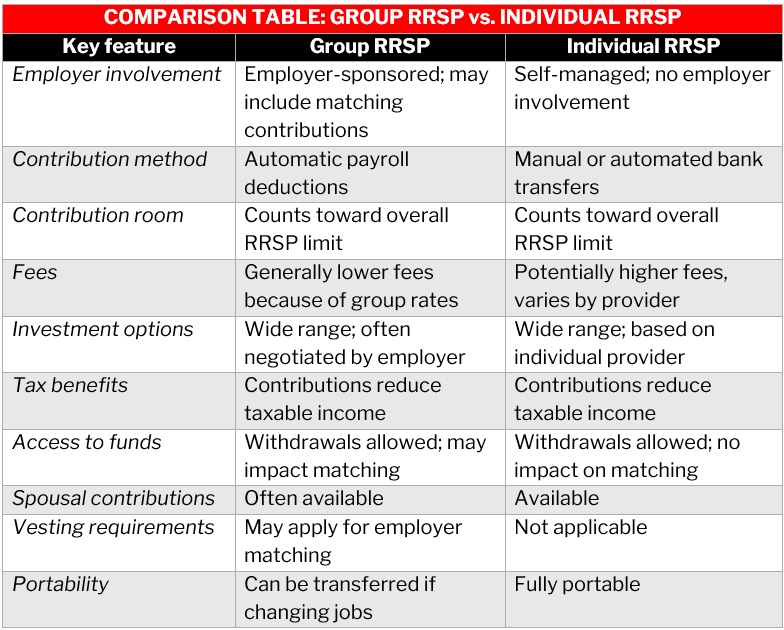

What is the difference between group RRSP and individual RRSP?

Group registered retirement savings plans share certain similarities with individual RRSPs, but there are also differences. Understanding what sets these plans apart is often key to maximizing your retirement savings.

Group RRSP vs. individual RRSP: similarities

- Tax-deferred growth: Both plans offer tax-deferred growth. This means your investments grow tax-free until you withdraw them.

- Contribution room: Contributions to group and individual RRSPs count toward your overall RRSP contribution limit set by the CRA. Overcontribution can result in tax penalties.

- Investment options: You can access a range of investment options for both plans. These can include mutual funds, bonds, and stocks. With group registered retirement savings plans, however, you may be bound by the options provided by your employer or the investment manager. Because of this, your choices may be limited compared to those with individual RRSPs.

Group RRSP vs. individual RRSP: differences

- Employer involvement: A group RRSP is offered through an employer, with features that include matching contributions that boost the employee’s savings potential. An individual RRSP doesn’t have this kind of employer involvement. The contributions are also entirely self-funded.

- Contribution process: Contributions to a group RRSP are made directly through payroll deductions. This makes the process easier and more convenient. With an individual RRSP, you make the contributions on your own, either through manual deposits or automated bank transfers.

- Fee structure: Group RRSPs often have lower management fees because they’re part of a larger plan negotiated by your employer. Individual RRSPs may come with higher fees that can eat into your savings.

- Accessibility and portability: Both plans allow for withdrawals, but group RRSPs may have specific conditions regarding employer matching or vesting that can impact the availability of funds.

Here’s a summary of the similarities and differences between an individual and a group registered retirement savings plan.

What are the pros and cons of a group registered retirement savings plan?

Deciding whether to participate in a group registered retirement pension plan can be easier when you’re aware of the advantages and disadvantages. Group RRSPs come with unique benefits that can help you save for retirement, but there are also certain drawbacks. Here’s a closer look at the plan’s pros and cons:

Pros of group RRSPs

- Employer matching: One of the standout benefits of a group RRSP is the option of your employer to add money to your RRSP based on how much you contribute. This feature can significantly increase your retirement savings without any additional costs to you.

- Convenient contributions: Contributions come straight out of your paycheque, making saving easy and automatic. You don’t have to worry about forgetting to transfer money or setting up deposits.

- Immediate tax savings: Contributions to a group RRSP are made before taxes are taken out of your paycheque, which reduces your taxable income right away. This means you’ll see instant tax savings, giving you more take-home pay.

- Lower administrative fees: Group RRSPs often have lower management fees than individual RRSPs because they’re part of a larger, employer-negotiated plan. Lower fees mean more of your money stays invested, helping your savings grow faster over time.

Cons of group RRSPs

- Limited investment choices: While group RRSPs offer a range of investment options, these choices are often limited compared to what’s available in individual RRSPs. This also means that you may not have as much control over your investments.

- Vesting periods for employer matching: Some group RRSPs require that you stay with your employer for a certain period before fully owning the matching contributions. If you leave early, you can lose out on some of that extra money.

- Potential early withdrawals: Unlike pension plans, group RRSPs allow you to withdraw funds at any time. While this may sound like a benefit, it can be a downside because it tempts you to dip into your retirement savings.

- Shared contribution limits: The contribution room for a group RRSP is shared with any other RRSPs you have. This can limit how much you can contribute across all your RRSPs, especially if you’ve already maxed out your limits.

Is joining a group RRSP worth it?

Participating in a group registered retirement pension plan offers advantages that can make it a valuable part of your retirement strategy. With features like employer matching, automatic payroll deductions, and immediate tax benefits, group RRSPs can provide a structured and efficient way to build retirement savings.

While there are some downsides, including fewer investment options and shared contribution limits, the advantages often outweigh these drawbacks. This is especially true if your employer offers matching contributions.

Group RRSPs simplify the saving process, reduce fees, and provide a boost to your retirement savings that can be hard to match on your own. If you’re looking for an easy and effective way to build your financial future, joining a group RRSP can be a good idea.

But as with every important financial decision, it’s best to consult an experienced industry expert to ensure that your choice aligns with your financial goals.

Check out our group retirement directory if you’re looking for retirement planning specialists. Many of these companies employ industry experts and offer advice and services to help you achieve financial security in retirement. By partnering with these specialists, you can be sure that your financial future is well taken care of.

Have you participated in a group registered retirement savings plan? How was the experience? Share your story in the comments.